Innovation. Disruption. That’s what Elon Musk and Tesla have become synonymous for — and for good reason. A recent claim made that Tesla would be able to reach production of 20 million vehicles per year before 2030, however, may be more of a stretch goal than a realistic number, as staff at Mining.com has recently pointed out.

Granted, when Elon Musk made the claim in September of last year, he added the caveat that the 20 million vehicles production number would require “consistently excellent execution.” It’s more than that, though — the limitations of material inputs, and, more specifically, the challenges associated with critical mineral resource supply, cannot be executed away.

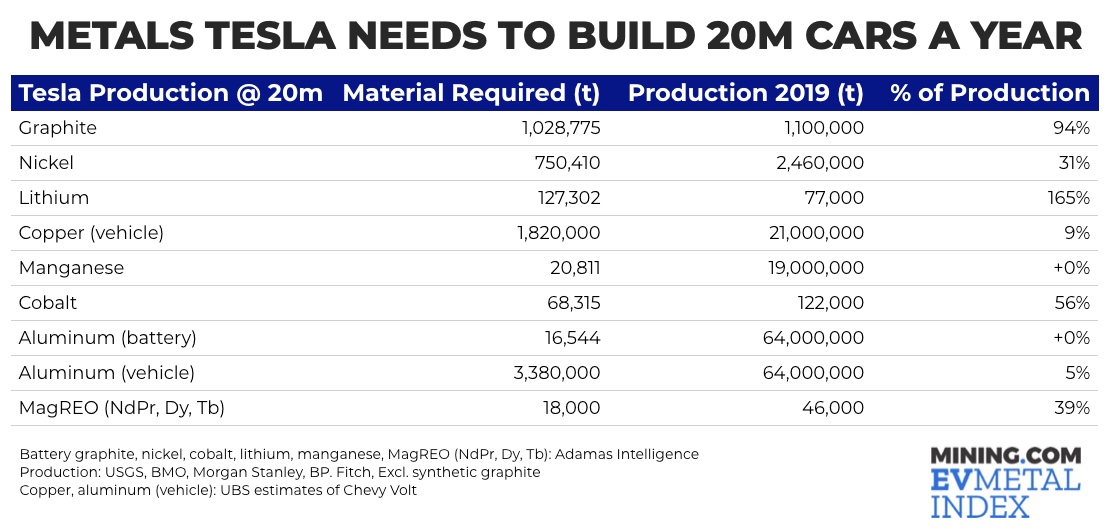

In an interesting thought experiment that puts these numbers into context, using data from Adamas Intelligence, Mining.com has extrapolated just how much in raw materials Tesla would require to produce those 20 million vehicles instead of the half million vehicles it produced last year.

Here’s the chart:

As Frik Els of Mining.com points out,

“When Tesla makes 20 million cars in a year it will need more than 30% of global mined nickel production in 2019 (2020 saw a 20%-plus reduction in output) for its batteries. Put another way, Tesla will have to buy the entire output of the top 6 producers – Norilsk, Vale, Jinchuan, Sumitomo, Glencore, BHP, and then some.”

Els continues, facetiously:

“Since Tesla is replacing graphite anodes with silicon, it’s not necessary to dwell on the fact that if this elusive scientific breakthrough is not commercialized at the speed of a Tesla in Ridiculous Mode, the carmaker would need 94% of the world’s natural graphite production by the time it hits 20 million cars a year. At least you can make more graphite.”

For cobalt, the requirement would be more than half of global production before 2030, and for lithium it would be a whopping 165%.

And, as followers of ARPN well know, rare earths may not in fact be “rare,” but that doesn’t mean they magically appear out of thin air like fairy dust.

While Mining.com’s number crunching and throwing shade may make Tesla’s numbers seem like pie in the sky constructs, they do underscore an important fact:

“The future energy system will be far more mineral and metal-intensive than it is today,” as Dr. Morgan Bazilian, Director of the Payne Institute and Professor of Public Policy, Colorado School of Mines testified before Congress in the fall 0f 2019, and several studies have since confirmed.

With the COVID-19 pandemic having underscored the challenges associated with the geopolitics of resource supply, and the green energy transition agenda having moved to the forefront under the new Biden Administration, securing and shoring up critical mineral resource supply chains is becoming increasingly paramount.