In a new piece for Canada’s Globe and Mail, Niall Mcgee discusses China’s quiet but systematic campaign to corner the critical minerals segment in Canada and stakeholder reactions in Ottawa, or more precisely, the lack thereof.

Citing the 2019 acquisition of the Tanco Mine in Manitoba, known as one of the world’s few sources of cesium as well as highest-grade lithium, by the Chinese Sinomine Resource Group, which earlier this year began shipping lithium produced at Tanco back to China to feed the country’s expansive EV industry, Mcgee laments that there has been little reaction from Ottawa:

“Although Ottawa has made clear that it does not want to be beholden to a hostile foreign power for critical minerals such as lithium, so far there has been little in the way of action from the federal government to prevent that from happening.”

Mcgee cites mining investor and activist shareholder Peter Clausi, who goes as far as calling the Canadian federal government, which could have initiated a review of the acquisition on national security grounds, “morons” for failing to do so:

“It’s [i.e. the Tanco Mine is] known for having the world’s highest grade lithium. The grade is so high that nobody had the technology to process it. And the morons let it go,” Clausi said.

As ARPN outlined in our discussion of the approval of the sale of Canadian lithium developer Neo Lithium Corp to Chinese state-owned Zijin Mining Group Ltd., in the process of which the Canadian government decided not to review the takeover on national security grounds:

“Foreign takeovers of Canadian companies are subject to an initial security screening by the government. If the initial screening concludes that the takeover constituted a threat to Canada’s national security, it would trigger a more formal review under Section 25.3 of the Investment Canada Act, and the deal could be blocked.”

In the case of Neo Lithium’s project – the 3Q Mine – the Canadian Government argued that “Canada was unlikely to benefit from lithium produced from Neo’s project, because it was located far away, in Argentina.” However, the project could have played an important role in supplying Canada’s lithium needs at a time when the country is not extracting the material within its own borders.

The same could be said for the Tanco deposit. As Mcgee elaborates, similar scenarios unfold for other metals and minerals:

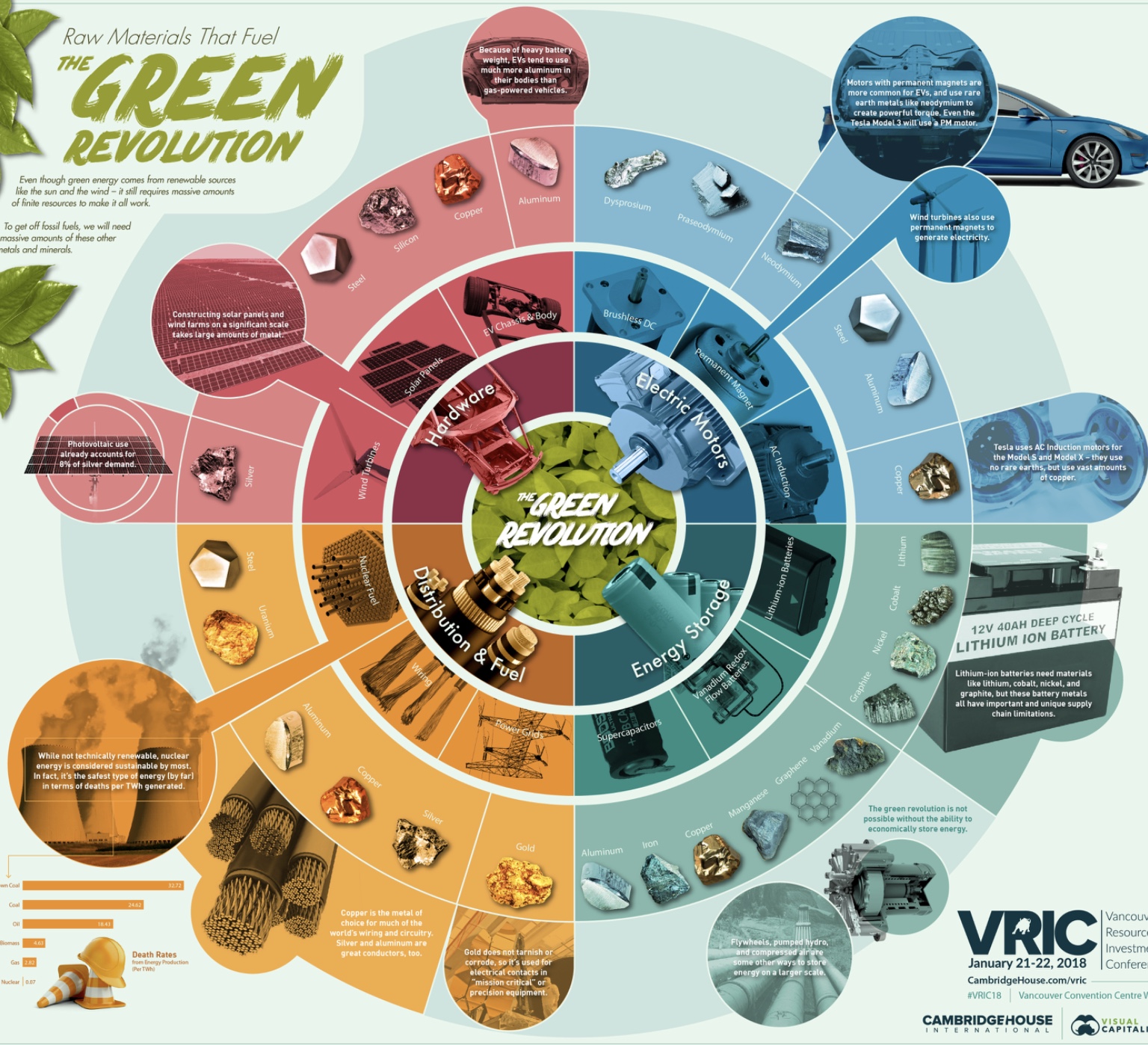

“Canada has similar also-ran status when it comes to cobalt. This country produces only small amounts of the vital battery metal input, while China controls about 70 per cent of the market. China is even more dominant in graphite, with an 80-per-cent lock on the market.

And while Canada is a major miner of nickel, another battery metal, it has no refineries that can process it for the battery industry.”

He cites Jeffrey Kucharski, adjunct professor at Royal Roads University and former assistant deputy minister of Alberta’s Department of Energy, who asked during parliamentary proceedings on the Neo Lithium deal:

“How can Canada build a lithium supply chain, or any other critical mineral for that matter, when it allows the assets of Canadian companies to be acquired by a country that seeks to cement its dominance in this sector?”

As ARPN previously outlined,

“the development ties into the broader North American context of the United States and Canada having formalized a joint action plan on critical minerals in 2020 which included commitments by both governments to strengthen North American battery material supply chains against the backdrop of China’s ever-tightening grip on global supplies.

A stronger focus on critical mineral resource security through the prism of national security is certainly warranted, not just for our Canadian friends, but also from a U.S. perspective.

As Tsvetana Paraskova notes in a piece for Oilprice.com, ‘while the Administration was reviewing supply chain issues and vulnerabilities to its demand for critical minerals, China is moving in on Africa and South America to strike alliances and lend money to mineral resource-rich African countries, while Russia is thought to be providing shadow ‘security services’ in some African nations with a mercenary organization with links to the Kremlin.’

Followers of ARPN know all too well that as the green energy transition accelerates, we will be facing significant critical mineral resource shortfalls. For the United States (and for our close allies), the time to act is now. As Paraskova concludes, ‘(…) otherwise, America’s clean energy goals and hi-tech and automotive supply chains could depend on China.’

The energy provisions in the just passed Inflation Reduction Act, coupled with a prior invocation of the Defense Production Act for the “Battery Criticals” – lithium, cobalt, graphite, nickel and manganese — are indications that the urgency of the situation has begun to resonate with U.S. policymakers.

Of course, as we cautioned in our latest piece on the Inflation Reduction Act, “any new law this wide-ranging will require federal guidance on the way to implementation – and spark follow-on efforts by resource development opponents to roll-back some elements even as resource development proponents look to build on this new legislative initiative.”

However, there is good reason to hope that “the bill’s requirements will help jumpstart a more comprehensive push towards domestic sourcing and processing, onshoring, friend-shoring, and harnessing the materials science revolution,” all of which would represent a “critically important leap forward to build the secure, responsible industrial base our economy and national security needs,” in the words of General John Adams, U.S. Army brigadier general (ret.).