In a new piece for Canada’s Globe and Mail, columnist Robert Muggah zeroes in on the geopolitics of mineral resource supply, which have, in his view, triggered a new “Great Game” – a term coined by British writer Rudyard Kipling to describe the “fierce competition between Victorian Britain and Tsarist Russia, both of which sought to control South Asia and Africa” which “went on to shape geopolitics for much of the rest of the 19th and 20th centuries.”

The new Great Game, according to Muggah, foreshadowed by the 2010 rare earths dispute between China and Japan, gained momentum with the adoption of the Paris Agreement in 2015 which committed countries to significantly reduce greenhouse gases and transition to renewables.

Writes Muggah:

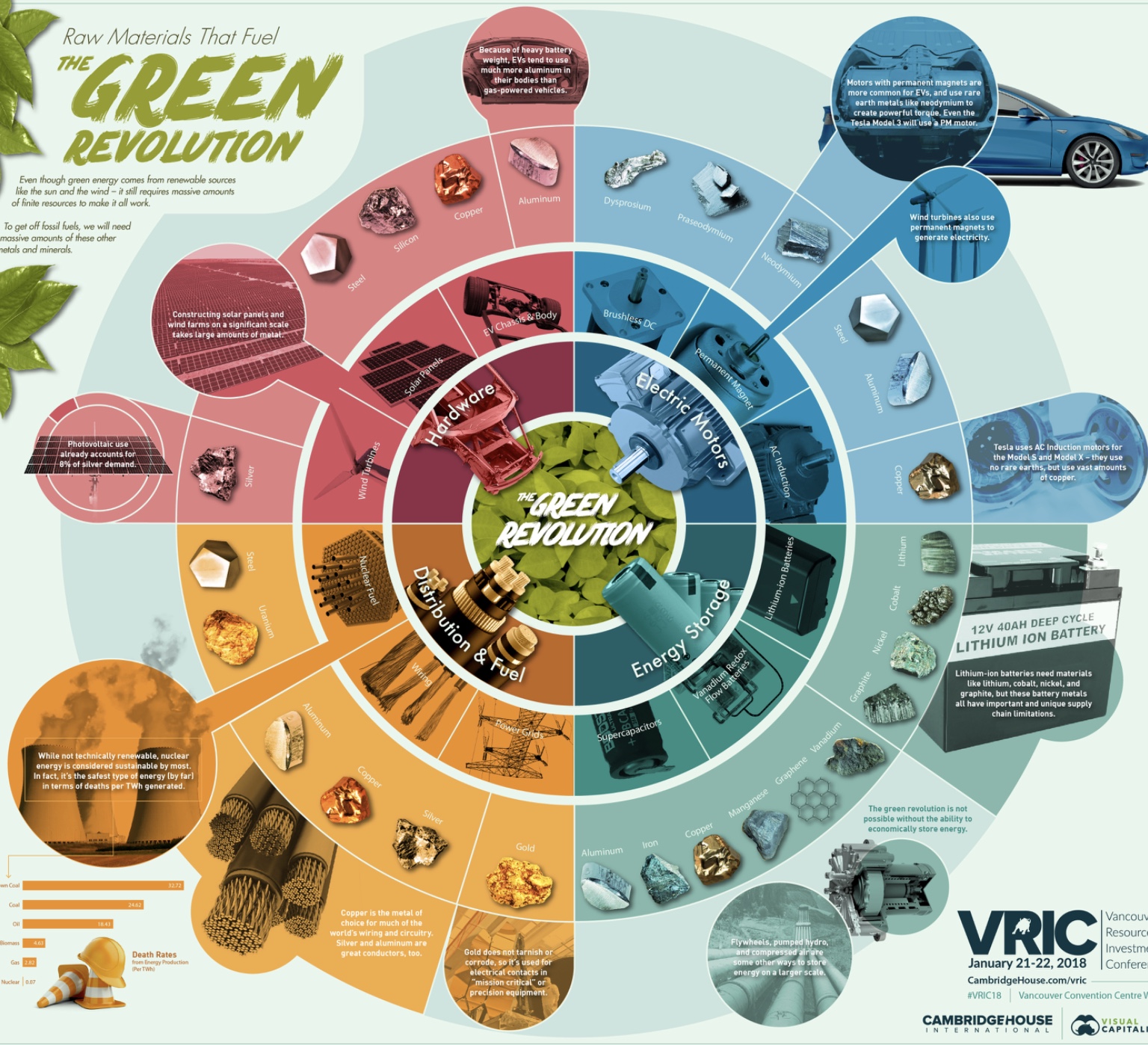

“In order to achieve the agreement’s targets by 2050, more than 60 per cent of installed power capacity will need to come from a combination of solar plants, wind farms, hydropower, bioenergy, geothermal reservoirs and batteries to power electric vehicles. But scaling these climate-friendly technologies comes with a catch: a sixfold increase in the sourcing of so-called critical minerals such as nickel, copper, lithium and cobalt as well as rare earths, by some estimates.

And so while the effort to move away from oil, gas and coal to low-carbon energy sources is essential, it has also unleashed powerful destabilizing forces. Countries are scrambling to secure the minerals needed to power the green transition; competition among major powers to control supply chains could trigger new global security risks.”

Muggah points to China as the undisputed dominant player “when it comes to refining those critical minerals and rare earths, effectively leveraging its state-backed firms, low-cost work force and lax environmental standards to gain a stranglehold on global markets.” Despite its omnipresence in global critical mineral supply chains, he says, China “does not yet dominate the exploration and extraction of critical minerals such as cobalt, lithium or nickel.” As a result, companies with backing from Beijing are “busily scouring international markets for raw materials, from Argentina, Bolivia and Chile to the Democratic Republic of Congo, South Africa and Zambia, but the competition is fierce.”

While Russia is another key player as one of the top producers of palladium, scandium, titanium and nickel, Russia’s war on Ukraine and subsequent sanctions against Russia have slowed down Moscow-backed domestic critical minerals production and processing and external pursuits, further consolidating China’s pole position in the global race for resources.

Muggah laments North American and Western European lack of expediency to build out their own critical mineral supply chains, not least due to most Western countries facing “major hurdles when it comes to accelerating domestic and international production and processing of critical minerals and rare earths, including the high costs of capital investments, long lead times to build out mines and refineries, and stronger environmental and labour standards compared to countries such as China and Russia.” However, he says, “supply chain disruptions during the COVID-19 pandemic, the war in Ukraine and rising tensions with China – including Chinese threats to curb rare-earth exports to the U.S. – have all served as a wake-up call,” and a new Great Game is on.

He goes on to detail recent steps taken by the U.S. and European Union to diversify its supply chains away from adversaries in general, and China in particular, which both appear to embrace a comprehensive “all-of-the-above” strategic approach, ranging from strengthening domestic production, over strengthening closed-loop concepts to increased “friend shoring.”

In this context, Muggah believes Canada “will have a consequential role to play in what is shaping up to be one of the defining struggles of our era,” and goes on to discuss Canada’s latest policy initiatives to strengthen critical mineral supply chains.

Muggah says there is reason for “cautious optimism that Canada can achieve its goals,” but that “Canada and its partners still face major obstacles to meet their ambitions, including from China.” He points to Chinese firms having acquired several key Canadian mines (see ARPN’s recent post on the issue here) and calls for greater scrutiny for mining deals with state-owned mining companies from authoritarian countries, arguing that “Canada will need to broaden its conception of what constitutes national security in relation to critical minerals and rare earths.”

He closes:

“To achieve more strategic autonomy amid the new Great Game, Canada must build more predictable and sustainable supply chains and take a more pro-active global role in driving the global shift to renewable energy. (…) Notwithstanding China’s firm grip on global supply chains of critical minerals and especially rare earths, Canada and its allies can support a more predictable green transition.

This is one game that Canada can and must help the whole world win.”

The question for the United States, where the midterm elections — and with that intensified partisan politics — are just around the corner, is whether policy makers will maintain their newly gained bipartisan focus on the importance of critical mineral supply chains and continue to work towards achieving greater mineral resource independence.